Blockchain – a technology that everyone is talking about, yet everyone has many questions about. If understanding blockchain technology feels insanely difficult right now, try thinking of it as explaining how the internet works to someone way back in the 60’s. It seemed mythical then, but today, it’s everywhere.

That is just how ubiquitous blockchain technology is going to be in the next few years, just as commonplace in our everyday lives.

That is why if you are someone who like to invest in futuristic technology, an analyst, trader, business person, manager, or even a tech savvy enthusiast, this blogpost will help you in understanding block chain – how it works, why there’s a need for it, what its advantages are, and what businesses can benefit from blockchain technology.

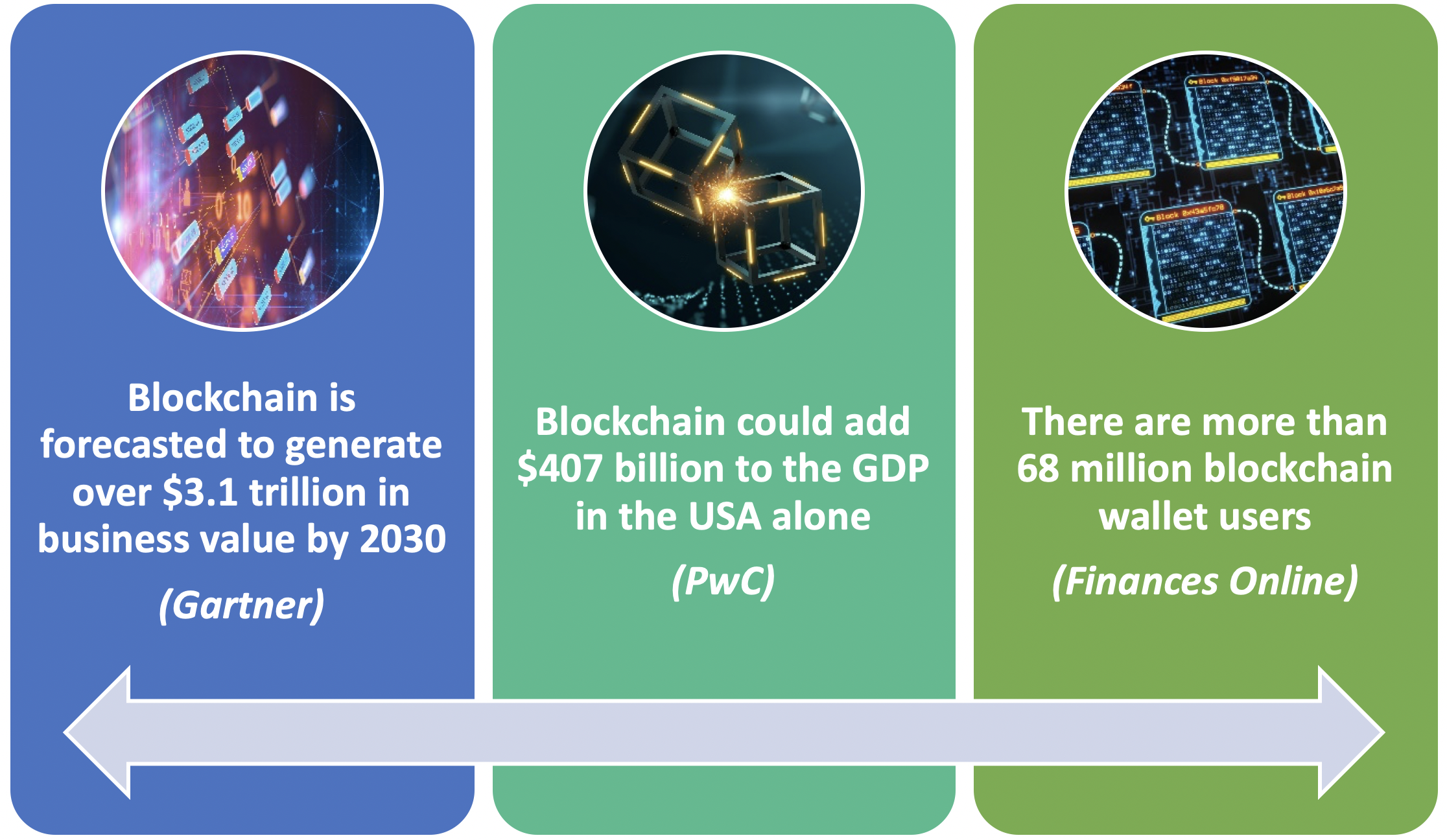

Sources: Gartner, PwC, Finances Online

What is blockchain?

Let’s begin by understanding the very basic question first. What is blockchain?

Blockchain is a highly secure and transparent system of recording information in a way that the said information cannot be changed, edited, hacked, or defrauded. Thus, a blockchain is essentially a ledger of information that is distributed across a network of many computers. As the data is stored in different blocks in different computers, no hacker can have it all from any one or even a few computers. That’s what makes blockchain technology so secure.

All data stored in blockchain is encrypted end-to-end, making it that much more secure.

Who owns blockchain?

More importantly the thing that makes blockchain technology so powerful is the fact that it is decentralized. This means that no one person or entity owns it. Every bit of data fed into the blockchain is owned by every member of that blockchain. This universal accountability is what gives blockchain a transparent and credible system.

In other words, nobody owns blockchain, just like the technology behind internet. Just like anyone can create a website on the internet, anyone can create a blockchain, and run it on the blockchain technology.

What can blockchain technology be used for?

Coming to the real matter at hand, what can we do with blockchain? In other words, what are real life applications of blockchain?

At the core of blockchain technology is trust. So anywhere there is a need for trust, there’s application of blockchain. So be it banking and finance, or healthcare, blockchain has far-reaching benefits. Let’s take a detailed look at how blockchain technology can help different industries.

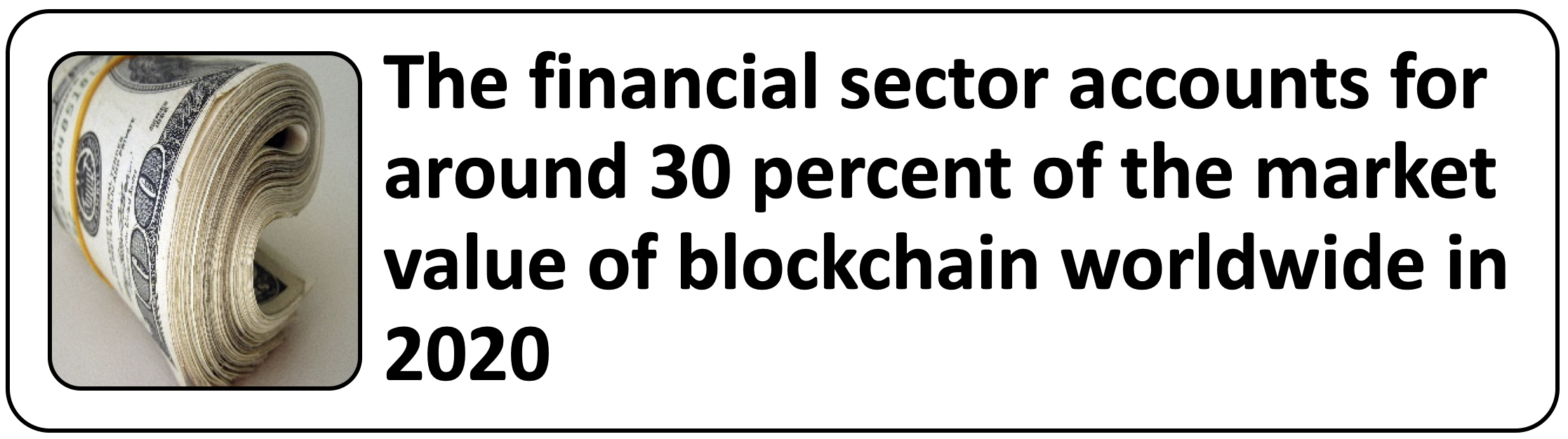

Blockchain benefits in banking and finance

Perhaps the most prominent use of blockchain is in banking and finance. Blockchain has the potential to revolutionize digital trust when it comes to exchanging money.

Every time you transfer money, be it a business transaction, or to family and friends, you go through a bank. Not only does the bank charge you a fee for most transactions, taking a bit out of your own money, but also there’s always a chance that someone at the bank knows everything about what you are doing with your money. Due to the rampant data breaches and lack of trust in traditional banking, people world over are reluctant to handover their personal life to the banks in this manner.

Blockchain steps in to help decentralize the banking process and place control your money in your hands. Blockchain technology can reduce friction, streamline processes, and lower costs in banking operations and financial transactions. With the added security and transparency, it makes digital transactions cheaper for consumers and less vulnerable to cheating and fraud.

Improved transparency – as blockchain uses the distributed ledger technology, it makes the financial industry more secure and transparent. As every transaction is monitored and verified by multiple sources on a public ledger, inefficiencies like fraud can be easily exposed thus reducing risk for financial transactions.

Added security – with the rapid increase in digital payments, users are increasingly vulnerable to theft, fraud, and scamming. Payments made using blockchain are highly secure, end-to-end encrypted, and more traceable as compared to traditional banking.

Lower costs – blockchain brings in significant savings for both consumers as well as financial institutions with the help of reduced bank fees and several other associated costs.

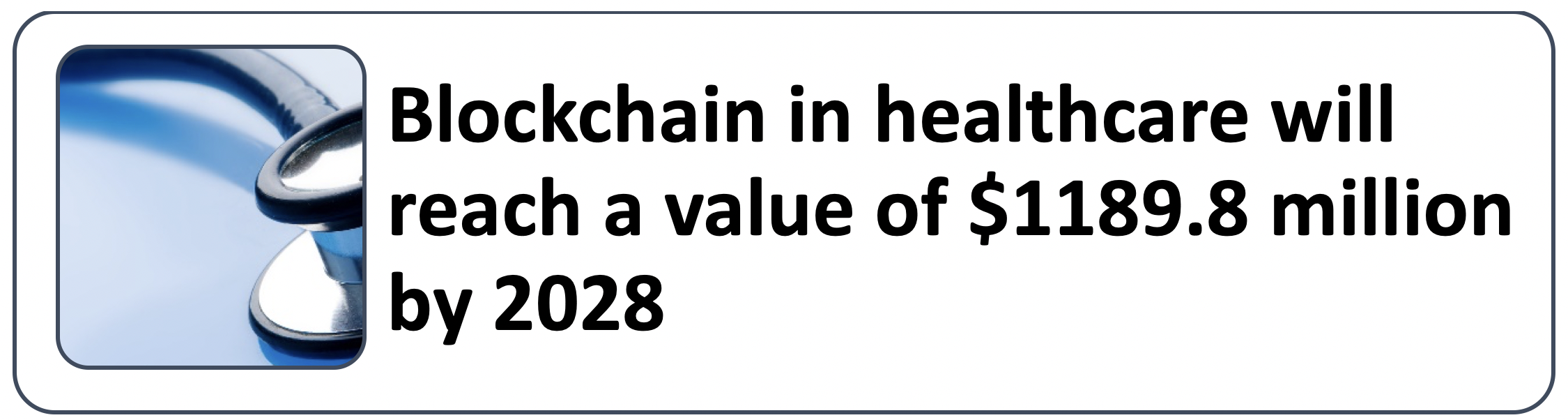

Blockchain applications in healthcare

Healthcare is another high priority, high sensitivity area. Blockchain applications in healthcare can serve multile benefits to overcome barriers and streamline processes. It can reduce friction and increase security in areas such as patient records management and easy patient transfers.

Improved patient care – for patients, keeping a well organized medical recors can be a difficult task. Test reports, prescriptions, dated visiting records, scans, diagnoses, payments and insurance papers, and so much more becomes overwhelming, especially considering the fact that patients already have physical and emotional stress to deal with.

Electronic health records have tried to make the situation better in the last few years but multiple data breaches have time and again exposed patient records opening a Pandora’s Box of cyber-attacks. With patient privacy under threat, blockchain can step up to make things better with its built-in security, end-to-end encrypting, and traceability.

Easy patient transfers – every time a patient moves or has to switch doctors for any reason, comprehensive patient history is necessary to ensure proper continuance of treatment. Once again, shuffling through paper trail is tedious and inadequate. Patient records saved with blockchain are sharable privately between the patients and doctors, ensuring seamless switching and uninterrupted treatment.

Tracking outbreaks – blockchain can help real-time disease reporting and analysis of disease patterns to detect outbreaks, trace its roots and monitor transmission, to help faster control and better management.

Blockchain benefits in supply chain management

Blockchain can help build trust between traders and vendors, enabling end-to-end visibility for increased transparency, thereby streamlining processes to resolve issues faster to build stronger supply chains.

Using blockchain to record price, date, location, certification, quality, and all other requisite parameters can help efficient management of the supply chain. The increased traceability offered by blockchain helps reduce risk and lower cost across the spectrum, driving high efficiency operations. This results in:

- Lower losses incurred due to spoilage, grey market trading or counterfeiting

- Increased adherence to standards thanks to enhanced traceability

- Improved visibility and compliance

- Reduced administrative work and minimal paperwork

- Improved credibility and higher trust

Types of blockchains

There are primarily four types of blockchains:

-

Public Blockchain

Public blockchains are decentralized networks of computers open to public. Anyone wanting to become a member of these blockchains can place a request online just as easily as creating an email account on the internet. Those who register become miners, and serve to validate transactions.

The most common examples of public blockchains include Bitcoin and Ethereum.

-

Private Blockchain

Private Blockchains are created by a certain individual or entity, and is hence centralized and access is restricted. B2b virtual currency exchange networks like Hyperledger and Ripple are examples of private blockchains.

-

Hybrid Blockchains or Consortiums

Consortiums are a combination of public and private blockchains. Essentially, they contain a mix of centralized and decentralized features. The lines between these are still quite blurred and many fail to even make a distinction between the two. Some examples are Energy Web Foundation, R3, and Dragonchain.

-

Sidechains

The fourth type of blockchains are Sidechains. A sidechain runs parallel to the main chain, allowing users to move digital assets to and from different blockchains to improve efficiency and scalability. An example is Liquid Network.

How does a public blockchain and Bitcoin Mining work?

Of the four types of blockchains above, the one you can relate most to is the public blockchain. This is the one that cryptocurrency miners use. As we mentioned, Bitcoin and Ethereum are the most popular public blockchains and also the most sought after cryptocurrencies. So let’s take a look at how it all happens.

What is Bitcoin?

Bitcoin is a digital currency that operates free of any central control by any banks or governments. Anyone can sign up to become a bitcoin miner by simply signing up to the public blockchain. As you know, any transaction entered into the blockchain needs to be verified by these users or miners.

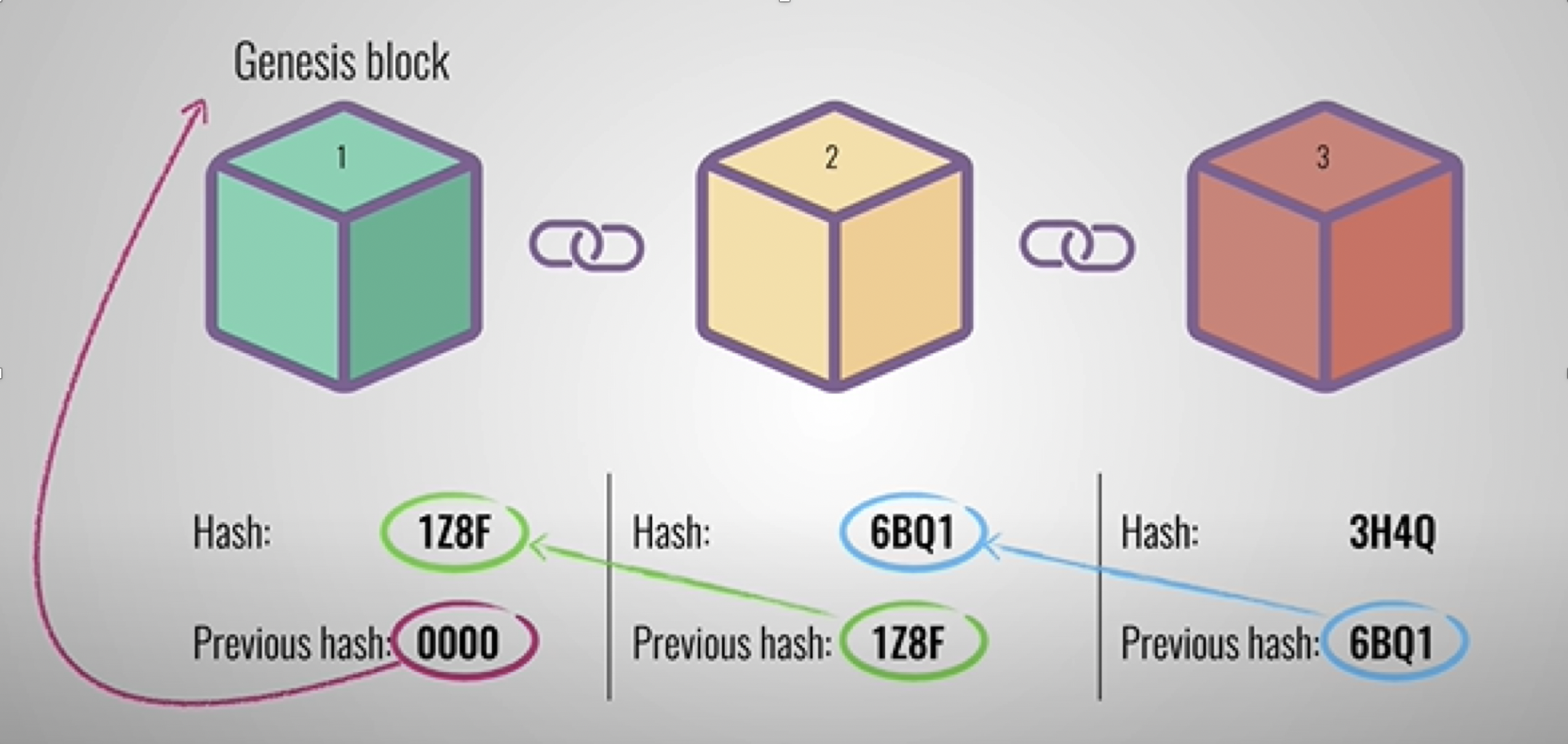

To understand how this happens, one must understand the basic structure of a blockchain.

Image source: https://medium.com/mobindustry/designing-a-blockchain-architecture-types-use-cases-and-challenges-9894fb7b58e

Every block has a unique hash, which is a collection of letters and numbers. The hash changes with every miniscule change made to the data in a block. The chain of blocks is interlinked as seen in the above image, where the hash of a new block corresponds to the previous hash of the preceding block. Now, if any change is made to any data in a block, its hash changes, thereby triggering a discrepancy with the next block. This way, any change made can be immediately detected, ensuring that no one can tamper with the data entered in a blockchain.

Now, to keep this entire system working, we need people (or miners) who volunteer to check every single block of data to verify that it hasn’t been tampered with. This involves special type of software and hardware with high computing capabilities. Anyone entering their information into the blockchain pays a fee, which is in Bitcoin. The miners who complete verifying a complete block receive a certain amount of bitcoin as their reward. This is essentially how miners work hard to keep the blockchain secure and in turn earn Bitcoin for themselves.

Conclusion

We hope that this article helped you get a grip on the basics of blockchain. In essence, blockchain is a type of secure database that has vast applications in various industries. As digital transactions take center stage in world economy and even as cyber threats grow, blockchain can help increase digital trust, safeguarding data across industries.

Understanding blockchain also opens up a world of investment opportunities as well as business ideas. Bitcoin Mining is growing in popularity and this post can be a starting point to help you how that works too. You can also become a blockchain developer and use your strong development skills to build secure blockchain architectures for businesses.